Every investor normally has personal goals in mind that they would like to achieve. Although most non-retired adults have some savings, only 36% say their nest egg is “on track,” according to the Federal Reserve. Sometimes, those eager to boost retirement savings could become more aggressive and start considering more volatile assets in an attempt to achieve higher returns. Sadly, this might be a recipe for a huge disappointment. Discipline has always played a fundamental role in investing and many best practice approaches start by having investors define their personal goals.

(Source: CNBC 6/27/2021)

Knowing what your goals are is traditionally the first step to achieving them. The second step is creating a plan that is best suited to reach those goals. The third, and hardest part, is sticking to that plan even through volatile and uncertain times. It is easy to forget about your financial plan and focus on other aspects of your life when things are going well. However, when inevitable fluctuations or market moves arrive, even the steadiest investors could become nervous and veer off course.

Volatility in both equity and bond markets is part of the investing experience. Although historically, stocks have provided higher long-term returns than bonds or short-term investments, stock prices are not destined to move in a straight line. Understanding what you can, and perhaps more importantly, what you cannot control in the investing world, can help even the savviest investor better weather any storms that arrive.

Three things an investor can control are:

1.Your risk tolerance or appetite;

2.Your time horizon; and

3.Your behavior.

If you have a firm grasp of each of these, you should be able to maintain discipline and remain calm when volatility and market fluctuations arise.

Risk Tolerance or Appetite

Risk tolerance or appetite is the degree to which you are able or willing to withstand fluctuations in the stock market and your portfolio in return for growth potential. If your risk appetite is low, you will likely want to be a conservative investor. If it is high, you are more likely to take more aggressive moves and accept any potential downside.

Knowing what your risk appetite is and having risk awareness should be a part of your financial strategy. Four good questions to ask yourself to assess your risk tolerance are:

1.What is my overall financial position?

2.What is my time horizon?

3.Do I have the financial ability to endure market declines?

4.How will I emotionally react to market volatility?

It is important that you determine your risk appetite before making investment choices. Considering your comfort level, emotional capacity to ride out volatility, and your time frame for investing before making your final decisions is crucial when implementing your financial plan.

As your financial professional, one of our primary goals is to help you create a plan that considers your risk appetite If you are not sure what your risk appetite is, call us so we can assess your situation and determine this with you.

Time Horizon

Your time horizon is another vital component that you can control. Knowing how much time you have to reach your goals will help you determine other key elements like your risk tolerance. While no one can determine what will happen in equity markets during either the short- or long-term, if your horizon is longer, you may have more choices or a willingness to take on more risk. An investor who can commit to a 10-year time horizon can consider different selections, as compared to someone who needs to use that money in six months.

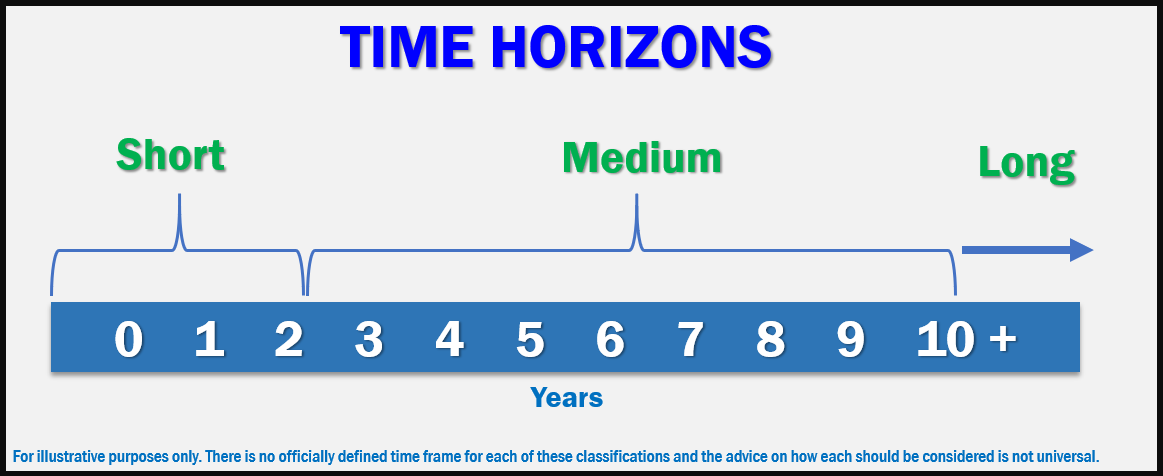

Generally speaking, the investor time horizon can be simplified to three major classifications: short, medium, and long. Please keep in mind there is no officially defined time frame for each of these classifications and the advice on how each should be considered is not universal.

Short term: two years or less

Medium term: two to ten years

Long term: ten years or more

Determining what your time horizon is will allow you to develop a plan around that timeline. While long-term investing typically could give you a better chance at minimizing any anxieties that could be caused by short-term market noise or volatility, some investors can have a medium- to short-term horizon. No matter what your time horizon is, we suggest focusing on your personal timeline instead of trying to time the market.

By helping you determine what your specific time horizons are, we can help you establish a financial strategy that is best suited to help you pursue your goals.

Investor Behavior

While you can determine your risk and time horizons, ultimately, your ability to emotionally endure the ups and downs of your investments will be a primary factor. A foundational rule of investing behavior is, don’t panic! In times of market volatility, many investors tend to become unnerved and anxious. This is usually not the best mindset to make rational decisions. Instead of making an emotion-based decision, three questions you need to ask yourself are:

1.Have my financial timelines changed?

2.Have my financial goals changed?

3.Has my risk tolerance changed?

Our goal is to help clients avoid making impulsive investing decisions. If you answer “yes” to any of these questions, we suggest you call us to discuss those changes before making any decisions.

We want to make sure you are comfortable with your investments. Equity markets will always have the potential to move up and down. Even if your time horizons are long, short-term downward movements in your portfolios are possible. Make sure your investing plan is centered on your personal goals and timelines.

Conclusion

Risk tolerance, time horizon, and your behavior should all be considered when investing. Many investors may feel they have the emotional fortitude to withstand volatility, however, they may not have the financial stability to ride it out. Conversely, some investors may have the financial stability and time horizon but simply have a high aversion to any sort of financial loss or fluctuations.

As your financial professional, we take all these key elements into consideration when assessing your financial pictures and determining a plan that gives you the best chance to achieve your goals. We are always available to revisit your financial holdings to make sure they are still compatible with your timeline goals and risk tolerance.

As a reminder, please keep us apprised of any changes (such as health issues or changes in your retirement goals). The more knowledge we have about your unique financial situation the better equipped we will be to best advise you.

We pride ourselves in offering:

- consistent and strong communication,

- a schedule of regular client meetings, and

- continuing education for every member of our team on the issues that affect our clients.