One of our main goals as holistic financial advisors is to help our clients recognize tax reduction opportunities within their investment portfolios and overall financial planning strategies. Staying current on the ever-changing tax environment is a key component necessary to help our clients benefit from potential tax reduction strategies.

One of our main goals as holistic financial advisors is to help our clients recognize tax reduction opportunities within their investment portfolios and overall financial planning strategies. Staying current on the ever-changing tax environment is a key component necessary to help our clients benefit from potential tax reduction strategies.

This report focuses on what individual taxpayers can potentially do to save money on their 2019 taxes. The Tax Cuts and Jobs Act (TCJA) enacted in 2017 brought many changes to the tax code. One big uncertainty is what will happen to the Tax Code after 2025. The way the Tax Cuts and Jobs Act is set up, the changes to the corporate side of the tax code are permanent, but the individual tax changes are mostly set to expire after the 2025 tax year. Unless indicated otherwise, TCJA provisions discussed here took effect in 2018 and are currently set to expire after 2025.

The objective of this report is to share strategies that could be effective if considered and implemented before year-end. Please note that this report is not a substitute for using a tax professional. In addition, many states do not follow the same rules and computations as the federal income tax rules. Make sure you check with your tax preparer to see what tax rates and rules apply for your particular state.

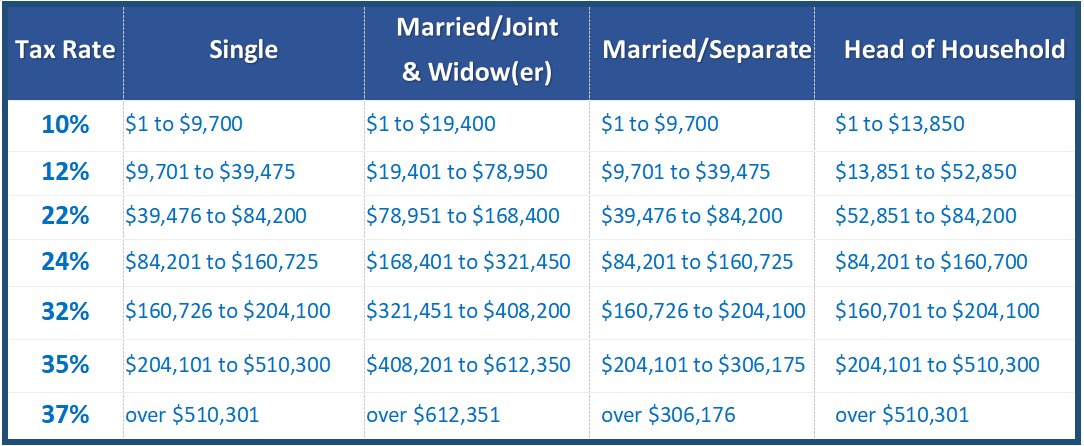

Income Tax Rates for 2019

For 2019 there are seven tax rates. They are 10%, 12%, 22%, 24%, 32%, 35%, and 37%. Under current laws this seven-rate structure will phase out on January 1, 2026.

Year-end Tax Planning for 2019

Last year ushered in many new tax laws and new tax forms stemming from the 2017 Tax Cuts and Jobs Act (TCJA). One of our primary goals is to help our clients optimize their tax positions. This report offers many suggestions and reviews strategies that can be useful to achieve this goal.

Last year ushered in many new tax laws and new tax forms stemming from the 2017 Tax Cuts and Jobs Act (TCJA). One of our primary goals is to help our clients optimize their tax positions. This report offers many suggestions and reviews strategies that can be useful to achieve this goal.

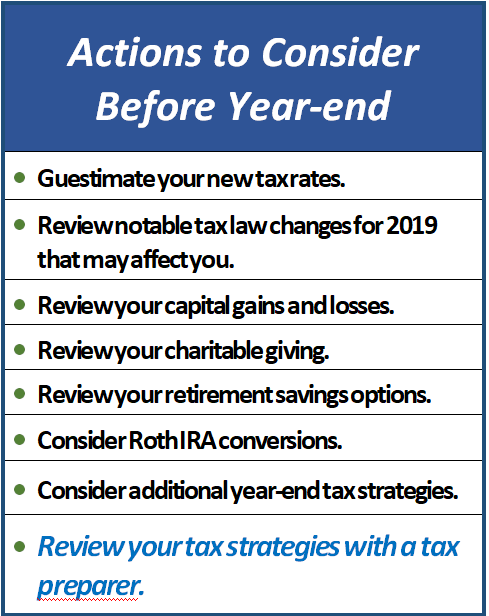

Everyone’s situation is unique, but it is wise for every taxpayer to begin their final year-end planning now!

Choosing the appropriate strategies will depend on your income as well as a number of other personal circumstances. As you read through this report you it could be helpful to note those strategies that you feel may apply to your situation, so you can discuss them with your tax preparer.

Some items to consider include:

— Evaluate the use of itemized deductions versus the standard deduction

For 2019, the standard deductions are $12,200 for singles and $24,400 for married filing jointly. This is up $200 and $400 respectively from 2018.

As a reminder, in 2018, the Tax Cuts and Jobs Act roughly doubled the standard deduction. It’s reported that this helped decrease many taxpayers bills in 2018 who typically claim this standard deduction. Although personal exemption deductions are no longer available, a larger standard deduction, combined with lower tax rates and an increased child tax credit, could result in less tax. You should consider running the numbers to assess the impact on your situation before deciding to take standard deductions. Depending on your results, you may even need to adjust your estimated quarterly tax payments or think about turning in a new Form W-4 to your employer.

The TCJA also eliminated or limited many of the previous laws concerning itemized deductions. An example is the state and local tax deduction (SALT), which is now capped at $10,000 per year, or $5,000 for a married taxpayer filing separately. Additionally, the Tax Cuts and Jobs Act temporarily eliminates miscellaneous itemized deductions subject to the 2% floor (like tax preparation fees and employee business expenses) and limits the home mortgage interest deduction to home acquisition debt of up to $750,000, or $375,000 for a married taxpayer filing separately.

— Consider bunching charitable contributions or using a donor-advised fund

For many taxpayers, the doubling of the standard deduction and changes to key itemized deductions resulted in them not itemizing in 2018. It was estimated that about 15 million filers used the charitable contribution write-off in 2018, a sharp decline from the 36 million who utilized it in 2017. (wsj.com 2/15/2019)

One way to still be able to utilize the tax advantages of charitable contributions is through a strategy referred to as “bunching”. Bunching is the consolidation of donations and other deductions into targeted years so that in those years, the deduction amount will exceed the standard deduction amount.

Another strategy is to consider using a donor-advised fund. A donor-advised fund, or DAF, is a philanthropic vehicle established at a public charity. It allows donors to make a charitable contribution, receive an immediate tax benefit and then recommend grants from the fund over time. Taxpayers can take advantage of the charitable deduction when they’re at a higher marginal tax rate while actual payouts from the fund can be deferred until later. It can be a win-win situation.

— Review your home equity debt interest

Homeowners can deduct mortgage-related interest on up to $750,000 worth of qualified loans (married filing jointly) or $375,000 (single filers) on homes purchased after December 15, 2017.

The changes under the TCJA law apply to all tax years between 2018 and 2025. Home equity lines of credit (HELOCs) are deductible as well, but only if the funds were used to buy or substantially improve the home that secures the loan. Please share with your tax preparer how the proceeds of your home equity loan were used. If you used the cash to pay off credit card or other personal debts, then the interest isn’t deductible, even if the payoff occurred prior to 2019.

— Revisit the use of qualified tuition plans

Qualified tuition plans, also named 529 plans, are a great way to tax efficiently plan the financial burden of paying for college. Earnings in a 529 plan could be withdrawn tax-free only when used for qualified higher education at colleges, universities, vocational schools or other post-secondary schools. However, they changed that so 529 plans can now be used to pay for tuition at an elementary or secondary public, private or religious school, up to $10,000 per year. Unlike IRAs, there are no annual contribution limits for 529 plans. However, there are maximum aggregate limits, which vary by plan. Under federal law, 529 plan balances cannot exceed the expected cost of the beneficiary’s qualified higher education expenses. Limits vary by state, ranging from $235,000 to $529,000. Some states even offer a state tax credit or deduction up to a certain amount. If you are paying tuition for children or grandchildren to attend elementary or secondary schools, it might be advantageous to set up or revisit a 529 plan. This is also a strategy that can reduce your estate. If you want to explore setting up a 529 plan, call us.

— Maximize your qualified business income deduction (if applicable)

One of the most talked about changes from the Tax Cuts and Jobs Act was the new qualified business income deduction under Section 199A. Taxpayers who own interests in a sole proprietorship, partnership, LLC, or S corporation may be able to deduct up to 20 percent of their qualified business income. Please be careful, because this deduction is subject to various rules and limitations.

There are planning strategies to consider for business owners. For example, business owners can adjust their business’s W-2 wages to maximize the deduction. Also, it may be beneficial for business owners to convert their independent contractors to employees where possible, but before doing so, please make sure the benefit of the deduction outweighs the increased payroll tax burden and cost of providing employee benefits. Other planning strategies can include investing in short-lived depreciable assets, restructuring the business, and leasing or selling property between businesses. This piece of tax legislation would take an entire report to discuss, so we recommend that if you are a business owner, you should talk with a qualified tax professional about how this new Section 199A could potentially work for you.

Consider All of Your Retirement Savings Options for 2019

If you have earned income or are working, you should consider contributing to retirement plans. This is an ideal time to make sure you maximize your intended use of retirement plans for 2019 and start thinking about your strategy for 2020. For many investors, retirement contributions represent one of the smarter tax moves that they can make. Here are some retirement plan strategies we’d like to highlight.

401(k) contribution limits increased. The elective deferral (contribution) limit for employees under the age of 50 who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is $19,000, up from $18,500. The catch-up contribution limit for employees aged 50 and over who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan remains at an additional $6,000 ($24,500 total). As a reminder, these contributions must be made in 2019.

IRA contribution limits unchanged. The limit on annual contributions to an Individual Retirement Account (IRA) is $6,000, up from $5,500. This is the first adjustment to IRA contribution limits since 2013. The additional catch-up contribution limit for individuals aged 50 and over is not subject to an annual cost-of-living adjustment and remains $1,000 (for a total of $7,000). IRA contributions for 2019 can be made all the way up to the April 15, 2020 filing deadline.

Higher IRA income limits. The deduction for taxpayers making contributions to a traditional IRA is phased out for singles and heads of household who are covered by a workplace retirement plan and have modified adjusted gross incomes (MAGI) of $64,000 and $74,000 for 2019. For married couples filing jointly, in which the spouse who makes the IRA contribution is covered by a workplace retirement plan, the income phase-out range is $103,000 to $123,000 for 2019. For an IRA contributor who is not covered by a workplace retirement plan and is married to someone who is covered, the deduction is phased out in 2019 as the couple’s income reaches $193,000 and completely at $203,000 for 2019. For a married individual filing a separate return who is covered by a workplace retirement plan, the phase-out range is $0 to $10,000 for 2019. Please keep in mind, if your earned income is less than your eligible contribution amount, your maximum contribution amount equals your earned income.

Increased Roth IRA income cutoffs. The MAGI phase-out range for taxpayers making contributions to a Roth IRA is $193,000 – $203,000 for married couples filing jointly (up from $189,000 to $199,000 in 2018). For singles and heads of household, the income phase-out range is $122,000 – $137,000 (up from $120,000 to $135,000 in 2018). For a married individual filing a separate return, the phase-out range is $0 to $10,000 for 2019. Please keep in mind, if your earned income is less than your eligible contribution amount, your maximum contribution amount equals your earned income.

Larger saver’s credit threshold. The MAGI limit for the saver’s credit (also known as the Retirement Savings Contribution Credit) for low- and moderate-income workers is $64,000 for married couples filing jointly in 2019, $48,000 for heads of household and $32,000 for all other filers.

Be careful of the IRA one rollover rule. Investors are limited to only one rollover from all of their IRAs to another in any 12-month period. A second IRA-to-IRA rollover in a single year could result in income tax becoming due on the rollover, a 10% early withdrawal penalty, and a 6% per year excess contributions tax as long as that rollover remains in the IRA. Individuals can only make one IRA rollover during any one-year period, but there is no limit on trustee-to-trustee transfers. Multiple trustee-to-trustee transfers between IRAs and conversions from traditional IRAs to Roth IRAs are allowed in the same year. If you are rolling over an IRA or have any questions on this, please call us.

Roth IRA Conversions

Some IRA owners may want to consider converting part or all of their traditional IRAs to a Roth IRA. This is never a simple or easy decision. Roth IRA conversions can be helpful, but they can also create immediate tax consequences and can bring additional rules and potential penalties. Under the new laws, you can no longer unwind a Roth conversion by re-characterizing it. It is best to run the numbers with a qualified professional and calculate the most appropriate strategy for your situation. Call us if you would like to review your Roth IRA conversion options.

Capital Gains and Losses

Looking at your investment portfolio can reveal a number of different tax saving opportunities. Start by reviewing the various sales you have realized so far this year on stocks, bonds and other investments. Then review what’s left and determine whether these investments have an unrealized gain or loss. (Unrealized means you still own the investment, versus realized, which means you’ve actually sold the investment.)

Know your basis. In order to determine if you have unrealized gains or losses, you must know the tax basis of your investments, which is usually the cost of the investment when you bought it. However, it gets trickier with investments that allow you to reinvest your dividends and/or capital gain distributions. We will be glad to help you calculate your cost basis.

Consider loss harvesting. If your capital gains are larger than your losses, you might want to do some “loss harvesting.” This means selling certain investments that will generate a loss. You can use an unlimited amount of capital losses to offset capital gains. However, you are limited to only $3,000 ($1,500 if married filing separately) of net capital losses that can offset other income, such as wages, interest and dividends. Any remaining unused capital losses can be carried forward into future years indefinitely.

Be aware of the “wash sale” rule. If you sell an investment at a loss and then buy it right back, the IRS disallows the deduction. The “wash sale” rule says you must wait at least 30 days before buying back the same security in order to be able to claim the original loss as a deduction. The deduction is also disallowed if you bought the same security within 30 days before the sale. However, while you cannot immediately buy a substantially identical security to replace the one you sold, you can buy a similar security, perhaps a different stock, in the same sector. This strategy allows you to maintain your general market position while utilizing a tax break.

Sell worthless investments. If you own an investment that you believe is worthless, ask your tax preparer if you can sell it to someone other than a related party for a minimal amount, say $1, to show that it is, in fact, worthless. The IRS often disallows a loss of 100% because they will usually argue that the investment has to have at least some value.

Always double-check brokerage firm reports. If you sold a security in 2019, the brokerage firm reports the basis on an IRS Form 1099-B in early 2020. Unfortunately, sometimes there could be problems when reporting your information, so we suggest you double-check these numbers to make sure that the basis is calculated correctly and does not result in a higher amount of tax than you need to pay.

Zero Percent Tax on Long-term Capital Gains

You may qualify for a 0% capital gains tax rate for some or all of your long-term capital gains realized in 2019. If this is the case, then the strategy is to figure out how much long-term capital gains you might be able to recognize to take advantage of this tax break.

NOTE: The 0%, 15% and 20% long-term capital gains tax rates only apply to “capital assets” (such as marketable securities) held longer than one year. Anything held one year or less is considered a “short-term capital gain” and is taxed at ordinary income tax rates.

Some Notable Tax Changes for 2019

Some itemized deductions are affected in 2019 under the new tax laws. They include:

The floor for deductible medical expenses is increased to 10%. The Tax Cuts and Jobs Act lowered the threshold for medical expense deductions to 7.5% of Adjusted Gross Income AGI from the prior threshold of 10%, however, this change only was made for the 2017 and 2018 tax years. As of October 2019, the threshold is set to increase to 10% again unless Congress acts to extend it. The IRS on IRS.gov provides a long list of expenses that qualify as “medical expenses,” so it can be a good idea to keep keeping track of yours if you think you may qualify.

No more Obamacare penalties, starting in 2019. While Congress have thus far been unsuccessful in repealing the Affordable Care Act, the Tax Cuts and Jobs Act did eliminate the individual insurance mandate — aka the “Obamacare penalty.” This is the penalty you pay for not having health insurance. This penalty was repealed starting in tax years 2019 and beyond.

Some Notable Tax Changes That Continue in 2019

State and local income, sales, and real and personal property taxes (SALT) are still limited to $10,000.

Although existing mortgages are grandfathered in subject to the prior $1 million cap, interest expense on acquisition indebtedness for up to two homes is capped at $750,000 total for loans incurred after December 15, 2017 through 2025. Interest on home equity loans is not deductible after 2017 through 2025.

The deduction for casualty and theft losses is currently allowed only for presidentially declared disaster areas.

Miscellaneous itemized deductions disallowed after 2017 include: tax preparation fees, investment expenses, and unreimbursed employee expenses. Individuals with significant unreimbursed employee expenses, including mileage, internet/phone charges, and education costs should consider setting up an excludable working condition fringe benefit arrangement or accountable plan from their employers.

Alimony deduction changes. Under prior law, alimony and separate maintenance payments were deductible by the payor and includible in income by the payee. For divorce and separation instruments executed or modified after December 31, 2018, alimony and separate maintenance payments are not deductible by the payor-spouse, nor includible in the income of the payee-spouse. These changes will profoundly affect the structure of divorce settlements.

Alternative Minimum Tax (AMT) Changes

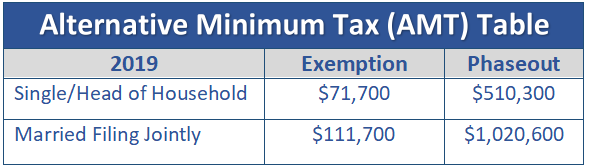

The AMT exemption amount for 2019 is $71,700 for singles and $111,700 for married couples filing jointly. The 28% AMT rate applies to excess Alternative Minimum Taxable Income (AMTI) of $194,800 for all taxpayers ($97,400 for married couples filing separate returns).

The AMT calculation can be complicated and you should discuss your situation with your tax professional, but here are some basic facts. AMT exemptions phase out at 25 cents per dollar earned once taxpayer AMTI hits a certain threshold. For 2019, the exemption will start phasing out at $510,300 in AMTI for single filers and $1,020,600 for married taxpayers filing jointly.

Other Family and Education Planning Changes

Child and family credit. The Child Tax Credit is $2,000 per qualifying child, with $1,400 of this amount being refundable. The TCJA of 2018 also adds a $500 nonrefundable credit for qualifying dependents other than children. More importantly, the act increases the phaseout for the child tax credit to $400,000 from $110,000 for married taxpayers filing a joint return and to $200,000 from $75,000 for other taxpayers.

Education benefits. The student loan interest deduction, education credits, exclusion for savings bond interest, tuition waivers for graduate students, and the educational assistance fringe benefit remain the same in 2019.

ABLE accounts. Contributions to ABLE accounts are now eligible for the retirement saver’s credit and a child’s 529 account can be rolled over to an ABLE account for the child.

Charitable Giving

This is a great time of year to clean out your garage and give your items to charity. Please remember that you can only write off these donations to a charitable organization if you itemize your deductions. Sometimes your donations can be difficult to value. You can find estimated values for your donated items through a value guide offered by Goodwill at https://goodwillnne.org/donate/donation-value-guide/

Send cash donations to your favorite charity by December 31, 2019 and be sure to hold on to your cancelled check or credit card receipt as proof of your donation. If you contribute $250 or more, you also need a written acknowledgement from the charity. If you plan to make a significant gift to charity this year, consider gifting appreciated stocks or other investments that you have owned for more than one year. Doing so boosts the savings on your tax returns. Your charitable contribution deduction is the fair market value of the securities on the date of the gift, not the amount you paid for the asset and therefore you avoid having to pay taxes on the profit.

Do not donate investments that have lost value. It is best to sell the asset with the loss first and then donate the proceeds, allowing you to take both the charitable contribution deduction and the capital loss. Also remember, if you give appreciated property to charity, the unrealized gain must be long-term capital gains in order for the entire fair market value to be deductible. (The amount of the charitable deduction must be reduced by any unrealized ordinary income, depreciation recapture and/or short-term gain.)

The law allowing taxpayers age 70½ and older to make a qualified charitable distribution (QCD) in the form of a direct transfer of up to $100,000 directly from their IRA over to a charity, satisfying all or part of the required minimum distribution (RMD) was made permanent in 2015. If you meet the qualifications to utilize this strategy, the funds must come out of your IRA by your RMD deadline (i.e. December 31, 2019).

Additional Year-end Tax Strategies and Ideas

Make use of the annual gift tax exclusion. You may gift up to $15,000 tax-free to each donee in 2019. These “annual exclusion gifts” do not reduce your $11,400,000 lifetime gift tax exemption. This annual exclusion gift is doubled to $30,000 per donee for gifts made by married couples of jointly-held property or when one spouse consents to “gift-splitting” for gifts made by the other spouse.

Help someone with medical or education expenses. There are opportunities to give unlimited tax-free gifts when you pay the provider of the services directly. The medical expenses must meet the definition of deductible medical expenses. Qualified education expenses are tuition, books, fees, and related expenses, but not room and board. You can find the detailed qualifications in IRS Publications 950 and the instructions for IRS Form 709 at www.irs.gov.

Contribute to a Qualified Tuition Plan (529 Plan) on behalf of a beneficiary. The effective annual contribution limit to 529 Plans for 2019 is $15,000. Transfers to 529 Plans count as annual exclusion gifts. Withdrawals (including earnings) used for qualified education expenses (tuition, fees, books and other related expenses) are income tax free. The tax law even allows you to give the equivalent of five years’ worth of contributions up front ($15,000 x 5 = $75,000) with no gift tax consequences. Earnings on non-qualifying distributions are subject to income tax and a 10% penalty. Overall contribution limits vary by state. Many states also provide contribution incentives such as tax deductions, tax credits or matching grants. If you’d like to learn more about what your state’s parameters are for 529 plans, please call us and we can assist you.

Make gifts to trusts. These gifts often qualify as annual exclusion gifts ($15,000 in 2019) if the gift is direct and immediate. A gift that meets all the requirements removes the property from your estate. The annual exclusion gift can be contributed for each beneficiary of a trust. We are happy to review the details with your estate planning attorney.

RMDs for those over 70½. One thing to watch closely by year-end is the RMD requirement. Most retirement arrangements (other than Roth IRAs) require that participants begin to take annual payments of benefits in the year they turn age 70½. While distributions generally must be made at the end of the calendar year, distributions for the first year can be delayed until April 1 of the succeeding year. If you have questions about your RMD, please call us.

Estate, Gift, and Generation-Skipping Tax Changes

Exemption amounts for gift, estate, and generation-skipping taxes for 2019 is $11.4 million, up from $11.18 million in 2018 ($22.8 million for couples), and the income tax basis step up/down to fair market value at death continues. These changes provide high net worth individuals a significant planning window to make gifts and set up irrevocable trusts.

As a reminder, as of now, the exemption amounts will revert in 2026 to 2017 levels (although the exemption amount has never decreased before), claiming the portable exemption will remain an important discussion topic for decedents with more than $3 million in assets.

Conclusion

One of our primary goals is to keep clients aware of tax law changes and updates. This report is not a substitute for using a tax professional. Please note that many states do not follow the same rules and computations as the federal income tax rules. Make sure you check with your tax preparer to see what tax rates and rules apply for your particular state.

There are many other additional tax reduction strategies that will vary depending on your financial picture. We encourage you to come in so that we can review your particular situation and hopefully take advantage of those tax rules that apply to you. Also, there are some pending legislative proposals like the SECURE ACT which could change your tax planning direction. We will try to monitor impactful changes and as always, we appreciate the opportunity to assist you in addressing your financial matters and look forward to seeing you soon!

Note: The views stated in this letter are not necessarily the opinion of LPL Financial and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Please note that statements made in this newsletter may be subject to change depending on any revisions to the tax code or any additional changes in government policy. Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary. Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount is subject to its own five-year holding period. Investors should consult a tax advisor before deciding to do a conversion. Contents provided by the Academy of Preferred Financial Advisors, Inc. Reviewed by Keebler & Associates. © Academy of Preferred Financial Advisors, Inc. 2019.